When we have paid any expense and its benefit is to be availed in future, it is termed as unexpired or prepaid expenses.

How is unexpired insurance treated?

Since after the above cash payment entry directly to expense, there is no entry into the Unexpired Insurance (asset) account, the adjusting journal entry requires a debit to Unexpired Insurance (asset) in the amount of $550 to make the balance in the Unexpired Insurance (asset) account correct.

What is the meaning of unexpired insurance?

Unexpired insurance is an another term which is used for prepaid insurance. Prepaid insurance is deducted from the insurance premium expenses account in profit & loss account and shown in balance sheet as current assets. For example, if an insurance premium of Rs.

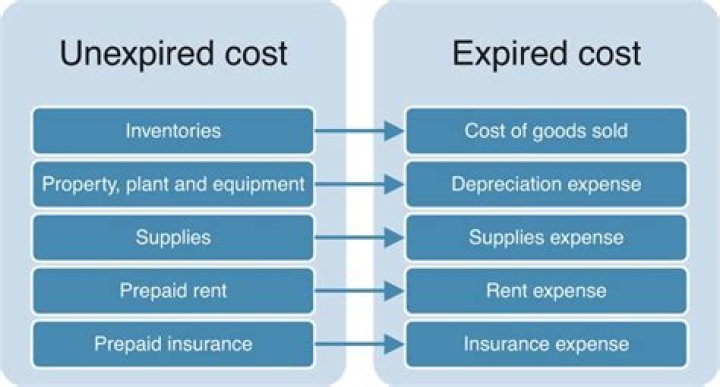

What is expired cost and unexpired cost?

Basically, when a cost is incurred, it could be in the form of deferred cost (asset) or expired cost (expense). Deferred costs are unexpired cost which provide benefit in the future periods. They are capitalised costs and known as assets and hence appear on the balance sheet.

How do you record unexpired expenses?

Unexpired expenses don’t affect cash flow because you’ve already paid for them. You report the expired portion of the prepayment on the income statement as an expense. You report the unexpired portion as an asset on the balance sheet.

Is unexpired insurance an expense?

Any insurance premium costs that have not expired as of the balance sheet date should be reported as a current asset such as Prepaid Insurance. Expired insurance premiums are reported as Insurance Expense. Unexpired insurance premiums are reported as Prepaid Insurance (an asset account).

Is expense expired cost?

An expired cost is a cost that has been recognized as an expense. This happens when an entity fully consumes or receives benefit from a cost (sometimes resulting in the generation of revenue). An expired cost may also be construed as the total loss in value of an asset.

What is period cost?

Period costs are all costs not included in product costs. Other examples of period costs include marketing expenses, rent (not directly tied to a production facility), office depreciation, and indirect labor. Also, interest expense on a company’s debt would be classified as a period cost.

What is the entry for prepaid expenses?

The initial journal entry for prepaid rent is a debit to prepaid rent and a credit to cash. These are both asset accounts and do not increase or decrease a company’s balance sheet. Recall that prepaid expenses are considered an asset because they provide future economic benefits to the company.

How do you record insurance expense?

Prepaid Insurance Journal Entry When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account. Thus, the amount charged to expense in an accounting period is only the amount of the prepaid insurance asset ratably assigned to that period.

Is prepaid expense an expired cost?

For example, a company spends $10,000 to acquire product catalogs, which it records as a prepaid expense in January. Instead, the $100 is charged to expense as incurred, which means it is an expired cost in June.

What should be recorded as an expense?

Under the accrual basis of accounting, an expense is recorded as noted above, when there is a reduction in the value of an asset, irrespective of any related cash outflow. The purchase of an asset may be recorded as an expense if the amount paid is less than the capitalization limit used by a company.

Which is an example of an unexpired expense?

Unexpired expenses, also known as prepaid expenses, are bills your business pays in advance. Suppose you pay your rent for the year on January 1 and also buy a full year of general liability insurance.

When does an insurance premium become an unexpired expense?

When we have paid any expense and its benefit is to be availed in future, it is termed as unexpired or prepaid expenses. For instance, when insurance premium is paid upto 31.3

When does an unexpired cost go on the books?

This cost is frequently associated with revenue that has not yet been recognized; under the matching principle, an unexpired cost is maintained on the books as an asset until the associated revenue is recognized, at which point the asset is charged to expense.

When to transfer unexpired expenses to an expense account?

At the end of the month, you transfer $1,000 out of assets to an expense account because you’ve used up the first month’s insurance. Unexpired expenses are treated differently from regular purchases because you don’t see an immediate reward for spending the money.